Nearing Retirement? Don?t Worry You Can Still Initiate Retirement Planning

As written on: 12th Feb, 2021

There is a misconception among young earners that one should start planning about retiring only when they cross the age of 40. But what these young individuals do not realize is that they are going to need more money to survive in their old age than they need today. Yes, keeping inflation in mind, the cost of living, medical expenses, the prices of almost everything are going to double by the time your hair turns salt and pepper. So if you decide to start saving and investing when you are young, you will actually have a lot of time in hand to accumulate wealth. When you are young time is your best friend. Unfortunately, youngsters do not realize the importance of saving when they are young.

Those who fail to realize the importance of investing early tend to regret it later. However, if you are one of those who turned their back on investing and are nearing retirement and feel that it’s too late to build a corpus, do not worry, you can still initiate retirement planning. Financial planning and investment planning go hand in hand. If you initiated financial planning at a young age, you might not have to worry about retirement planning later in life. That’s because the first step of financial planning is money management, which seems to be the problem with today’s young generation.

Money management is the simple task of taking care of all your expenses with your monthly income. But it doesn’t just end there. One needs to also make sure that they are also saving a certain portion of their monthly income so that they are able to slowly accumulate wealth for future financial sustainability. Some people follow a savings formula that is income – expenditure = savings. This formula is actually not the correct formula to follow. What happens is that most individuals spend all their earnings first and then save from whatever is left. This is not a healthy way to save. Expenses are usually driven by two things ‘needs’ and ‘wants’. Needs consist of basic necessities like food, shelter and clothing. To make it sound more contemporary, our monthly house rent, grocery bills, utility bills, travel expenses etc. are some of the expenses that are necessary and we cannot sustain without taking care of these expenses from time to time. The real problem is with our wants. We want a car to travel to work, a new smartphone every 6 months, new apparels, and dinners at fancy restaurants almost every week. How are you going to save when your unnecessary wants are surpassing your monthly income?

Remember that your outflow should never supersede your inflows. Because it will leave you looking for a lending hand at the end of every month and eventually you will end up with a credit card. Once your credit card bill starts piling up, there is no escape from that. Hence, to avoid this financial tragedy it is better that you revise the above stated formula by income – savings = expenditure. Yes, the moment you get your monthly salary, first decide how much you want to save and keep that money aside. Spend whatever is left. This way you will inculcate the discipline of saving regularly and will not have to worry about your long term goals.

Financial planning not only teaches you to manage money, but it also helps you determine your short term and long term financial goals. While our goal here is retirement planning, it usually requires investors to have a long term investment horizon. But since you are nearing retirement age, you do not have that much time. But do not worry even if you have 10 years in hand, through systematic investing you may be able to accumulate decent wealth. Investors are also expected to determine their risk appetite before investing their hard earned money in any type of financial scheme.

SEBI, the regulator of commodities and security in India, concluded mutual funds as a mechanism for pooling the resources by issuing units to the investors and investing funds in securities in accordance with objectives as disclosed in the offer document.

Investments in securities are spread across a wide cross-section of industries and sectors and thus the risk is reduced. Diversification reduces the risk because all stocks may not move in the same direction in the same proportion at the same time. Mutual fund issues units to the investors in accordance with the quantum of money invested by them. Investors of mutual funds are known as unitholders.

The profits or losses are shared by the investors in proportion to their investments. The mutual funds normally come out with a number of schemes with different investment objectives which are launched from time to time. A mutual fund is required to be registered with Securities and Exchange Board of India (SEBI) which regulates securities markets before it can collect funds from the public”

If you are keen on initiating retirement planning, follow these simple steps to make retirement planning even more effective:

Identify how much money you actually need: The most important thing while starting with retirement planning is to determine how much money you actually want to save. It is necessary for budding retirees to have a realistic amount in mind. Remember that if you have a realistic goal, then pursuing that goal might become easier. That’s because it will also help you understand how much money you need to save for initial investment.

Calculate your post retirement expenses: Just like identifying your retirement budget is essential, determining your average monthly expenses post retirement is equally necessary. If you have the habit of living on a low income budget right now, that is a good sign. This indicates you are well prepared to lead a life with fixed income when you retire. Because when you retire, your major source of income will mostly be a monthly pension plan and hence it is necessary to calculate your monthly expenses so that you save enough to take care of those expenses.

Try and put an end to all your debts: If you have any unpaid debts like credit card bills, unpaid loans, if you owe anyone money personally, it is important for investors to get rid of all these expenses before they retire. Retail investors should make sure that they aren’t riddled with any debt burdens. It is better to not owe money to any individual or financial institution as it might eat your retirement savings. The last thing you want is people and bank agents to knock on your door asking for money when you have retired and living on a fixed budget. So make sure that you do not owe anyone anything.

Identify how much income you’ll be drawing after your retirement: In case you have already invested in schemes like PPF or NPS, or if your office allows pension for its retirees, you need to know how much income you’ll be drawing from these sources. The income you’ll be drawing monthly or annually should be able to take care of your post retirement expenses.

The more you save the better it is: It is a given fact that irrespective of how much capital you save for your post retirement life, it is never enough. Because as we stated earlier, retirement is a phase where you’ll be withdrawing more than adding to your corpus. Thus, the more you save, the better it is. The last thing you want to do in your old age is to rely on estranged relatives or your children for financial favours. They might or might not be able to help you in case of an emergency. This is exactly why it is necessary for individuals to save enough so that they remain financially secured during your sunset years.

Start a SIP in a retirement fund: If you want to witness your savings turn into a wealthy corpus, you can consider starting a SIP in a retirement fund. A Systematic Investment Plan, abbreviated as SIP, is a mode to make an investment in mutual funds. Investors have the option of either going through lumpsum investment or they can opt for a mutual fund SIP. With SIP, one can invest small amounts at periodic intervals without having to deal with cash crunch. SIP is an easy and hassle free process to continue investing in retirement funds till your investment objective is achieved. All an investor has to do is instruct their bank, following which every month on a fixed date, a predetermined amount is debited from their savings account and electronically transferred to the retirement fund. The investor gets to decide the SIP amount they wish to invest on a monthly basis.

If you have an investment horizon of at least five years and are keen on investing in market linked schemes to build a decent retirement corpus, you can consider investing in Axis Retirement Fund.

Axis Retirement Fund is an open-ended retirement fund that unambiguously focuses on investors who are hoping to build a corpus that can allow them financial stability and security during their post-retirement life.

Axis Retirement Fund offers three investment plans -

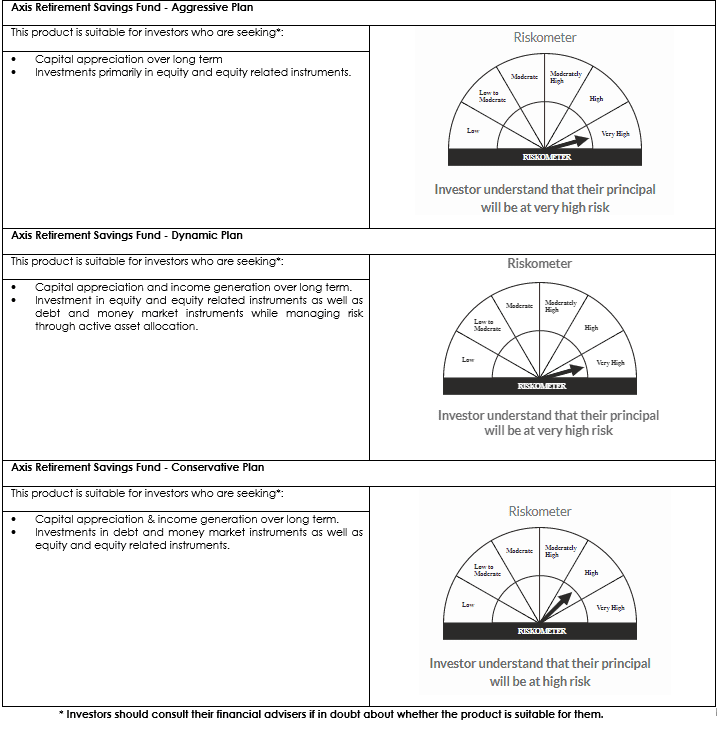

Axis Retirement Fund - Aggressive Plan: This plan can be opted by investors who are seeking capital appreciation with a long term investment objective. Here investments are predominantly made in equity and equity-related instruments as well as debt, money market instruments, Gold ETFs and units of REITs and InvITs. Investors who plan to opt for the Aggressive Plan can expect equity exposure anywhere from 65% to 80%.

Axis Retirement Fund - Dynamic Plan: This investment plan is brought into effect with a dual objective. Axis Retirement Fund - Dynamic Plan can generate capital appreciation by investing in equity and equity-related securities as well as generate income by investing in debt and money market securities. It manages to do this while attempting to manage risk from the market through active asset allocation. The Investment Plan may also invest in units of Gold ETF or units of REITs & InvITs for income generation.

Axis Retirement Fund - Conservative Plan: This investment plan by Axis Mutual Funds hopes to generate regular income through investments majorly in debt and money market instruments and to generate long term capital appreciation by investing a certain portion of the portfolio in equity and equity-related securities. Axis Retirement Fund - Conservative Plan may also invest in units of Gold ETF or units of REITs & InvITs for wealth creation.

Investors should bear in mind that the above plans differ in the varying degrees of equity and debt allocation and are suited for investors depending on their appetite for risk.

Axis Retirement Fund is a solution-oriented product aimed at building a wealthy retirement corpus for investors. This retirement fund can be considered by those who wish to lead a secure and financially stable life after retirement and also for those who want to indulge in their passions, hobbies, or venture on foreign trips in their sunset years.

These are some of the options that you may consider for initiating retirement. However, do bear in mind that investments made in mutual funds are exposed to market volatility. Hence, returns from these investments are never guaranteed. It is better that aspiring investors determine their risk appetite before making the actual investment so that they are able to make an informed investment decision.

Axis Retirement Fund

(An open-ended retirement solution oriented scheme

having a lock-in of 5 years or till retirement age (whichever is earlier)).

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Copyrights ![]() 2020. All rights reserved Axis Mutual Fund.

2020. All rights reserved Axis Mutual Fund.

Privacy | Terms | Disclaimer | Sitemap