Fund Focus - Axis Strategic Bond Fund Overview

Blended mix of AAA & Credit Instruments

Fund Manager: Devang Shah & Dhaval Patel

Brief Snapshot

- At Axis Mutual Fund, we have always followed a highly diversified portfolio

- No non AAA security more than 5%

- Top 10 securities constitute 34% of the portfolio

- Top 10 Non AAA constitute ~23% of the portfolio.

- No respective security lower than AA- rated form more than 2% of the portfolio.

- Our fund is positioned in short to medium space

- Typical maturity ranges of 2-4 years

- 40% of the assets to mature in less than 3 years

- 25% of the assets in less than 1-year bucket and no exposure of below AA- credits in more than 3-year bucket.

- Credit exposure is typically through short tenor instruments with frequent resets. This ensures frequent liquidity events in the portfolio

- High quality credits, has always been our focus

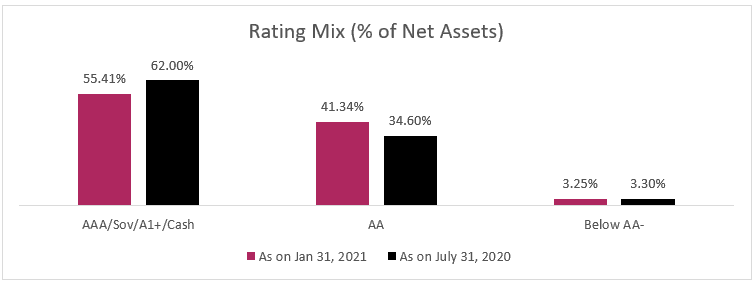

- 4% of the assets having AAA/SOV rating

- 41% of assets have rating AA category rating

- Only 3.3% of the portfolio is below AA-

- Lowest rating in our portfolio is A

- No exposure below A- rated security since inception of the fund

- No borrowing done in Strategic Bond Fund, since inception of fund

Portfolio Granularity

- Highly diversified corporate bond portfolio

- 67 unique instruments issued by 44 borrowers. Given the current fund size that amounts to an average of ~26 Cr per issuer or 2.27% per issuer.

- Detail Write-Up On Each Credit Is Provided Below

Top 10 Non AAA exposures

| Name of the Company | Rating | % of total AUM |

| Punjab National Bank | CRISIL AA+ | 3.03% |

| EPL Limited | CARE AA | 2.54% |

| G R Infra Projects Limited | CRISIL AA | 2.53% |

| PVR Limited | CRISIL AA | 2.52% |

| Pune Solapur Expressway Pvt Ltd | ICRA AA(CE) | 2.16% |

| Shriram Transport Finance Company Limited | CRISIL AA+ | 2.13% |

| Indian Bank | CRISIL AA | 2.13% |

| IndoStar Capital Finance Limited | CARE AA- | 2.13% |

| JK Cement Limited | CARE AA | 2.12% |

| Nuvoco Vistas Corporation Limited | CRISIL AA | 2.11% |

| Top 10 Non- AAA Exposures | 23% |

Credits below AA-

| Name of the Company | Rating | % of total AUM |

| Veritas Finance Private Limited | CARE A- | 1.44% |

| Northern Arc Capital Limited | ICRA A+ | 1.28% |

| Narmada Wind Energy Private Limited | CARE A+(CE) | 0.53% |

| Total Credits below AA- |

| 3.25% |

Maturity Profile - 40% of the fund with maturity less than 3 years

- Credit exposure is typically through short tenor instruments with frequent resets. This ensures frequent liquidity events in the portfolio

- 7% of the assets in less than 1-year bucket

- 55% of assets are invested in AAA/SOV papers; need based liquidity can be created by partly liquidating these assets

- Above 3 years no exposure below AA- papers

| Maturity Buckets (% of NAV) | As on January 31, 2021 |

| 0-1 years | 24.7% |

| 1-3 years | 19.3% |

| 3-5 years | 10.6% |

| Above 5 Years | 45.4% |

| Total | 100% |

Rating Profile – 96% of the assets with rating AA category and above

- Duration management is achieved through exposure in Sovereign/AAA Securities

Current Market View

Across our schemes today, portfolio positioning looks to play the ‘reinvestment theme’ and barbell strategies. We have consciously reduced portfolio maturities across our products in line with our view. Select long bond strategies continue to offer opportunities for investors looking to lock in long term rates.

In our short and medium duration strategies we are following barbell strategies – a strategy where we mix long duration assets (8-10 year) with ultra-short assets including credits (Up to 2 years) to build a desired portfolio maturity. The ultra-short assets will help us play the reinvestment trade whilst limiting the impact of MTM as yields rise. Long bonds will likely add value in capturing higher accruals with relatively lower credit risk and lower MTM movement in the current context.

The fund as part of its investment mandate aims to invest 50-60% in AAA bonds with overall portfolio duration target range of 2- 4 years. The spreads in short non AAA corporate bonds of 100-150 bps over AAA currently looks attractive from a risk reward basis and hence the fund is allocated assets to these securities on an incremental basis. The portfolio design should help generate stable returns while bringing down volatility relative to a longer duration fund. Currently, the fund has duration of 2.1 years.

Brief Write-up on Credits

EPL Ltd. (Earlier Essel Propack Ltd) (IND AA, CARE AA)

- The credit risk evaluation of EPL Ltd. (EPL) draws comfort from the strong promoter group. In August 2019 Blackstone group acquired controlling stake in the company.

- The Blackstone Group have taken control over the board of the company and has also recruited new MD and CEO.

- Assessment also factors in strong and established business risk profile of EPL characterized by dominant global position in laminated tubes business and increasing penetration in higher margin other packaging products used in pharma, personal care, foods etc.

- EPL has geographically diversified presence across Asia, Europe and Americas enabling it to cater to large FMCG clients in various geographies.

- EPL’s financial risk profile is marked by healthy profitability and strong cash flows resulting in improved capital structure (overall gearing of 0.51x times as on March 31, 2020) and debt coverage ratios (interest coverage ratio of 10.17 times as on March 31, 2020).

- As on September 30, 2020, the company’s cash and cash equivalents stood at around Rs.260 crores on a consolidated basis. The liquidity on balance sheet provides significant comfort to the overall financial risk profile.

G R Infraprojects (CRISIL AA)

- The company has also established manufacturing plants & capacities for raw materials used in road construction with a gross block of ~Rs. 1,500 Crs for road projects which is a positive

- Consequently, GRIL has a track record of completing projects ahead of schedule. Since 2013, 29 of 31 projects have been completed on or before time displaying efficient operations

- Healthy execution capabilities, owned fleet of equipment, sourcing tie-ups, and in-house designing and engineering teams have supported a 47% CAGR over the past five years

- GRIL has a healthy & diverse order book (over ~3x of its annual revenues) across 36 projects & 13 states as of Sep 30, 2020. This includes both EPC work (~58%) & HAM projects (~42%)

- Operating margin has been maintained at over 17% since FY17 which improved further to over 20% in FY19 and has been resilient despite challenging times during H1FY21

- GRIL’s consistent superior performance is a result of 3 factors: - (1) its selection of projects & counterparties. ~90% of the orders are from central government agencies thereby reducing counterparty risk, with 83% of the orders from NHAI, (2) Own road building material capacities & (3) financial resilience

- GRIL’s financial performance has been robust due to efficient scale of operations & decent WC management. The same has resulted in robust YoY performance on Operating cash flow enabling it to grow without piling on debt

PVR Limited (PVR; CRISIL AA)

- PVR Ltd. (PVR) is the largest multiplex operator in India with a strong brand equity.

- PVR has strong market position and established brand backed by healthy operating efficiency

- Addition of screens from SPI Cinemas Pvt. Ltd (SPI) has led to significant improvement in market position in South India and helped diversify content as South Indian cinema contributes more than 40% to the overall box office collections.

- Strong growth with improved operating performance due to consolidation in the industry; Low penetration levels provides large opportunity

- Strong financial risk profile with low leverage and strong debt protection metrics

- Film exhibition sector has been adversely impacted due to covid19 pandemic ; however, company has been able to maintain sufficient liquidity buffers by undertaking stringent cost controls, mobilising equity capital through rights issue of Rs.300 crores and also raising long tenure debt from various banks to take care of medium term liquidity requirements

- Various states have allowed theaters to starts operations since October 2020 with certain restrictions; overall ramp up of operations in next few quarters would be key monitorable in short to medium term

Pune Solapur Expressways Pvt. Ltd. [ICRA AA(CE)]

- Pune Solapur Expressways Pvt. Ltd. (PSEPL) is a 50-50 JV (SPV) between TRIL Roads Pvt Ltd and Atlantia SpA

- TRIL Roads is owned 100% by Tata Realty & Infrastructure Ltd (TRIL) which is further a 100% subsidiary of Tata Sons Pvt Ltd. Atlantia Spa. is one of the largest Listed concessionaire entity in Europe

- PSEPL was set up for developing and managing the project (toll road) for 4-laning of Pune Solapur section of NH 9 from 40 km to 144 km in state of Maharashtra under National Highway Development Program Phase III on Design, Build, Finance, Operate and Transfer (Toll) (DBFOT) basis.

- It is an operational project which achieved COD in January, 2015. It is a NHAI concession for a period of 21 years from November, 2009

- While some part of the debt is dependent on toll revenues (NCDs rated AA- currently), the remaining debt is 100% backed by TRIL’s corporate guarantee (rated AA(CE)

- Credit assessment for PSEPL NCDs in our portfolio factors in unconditional and irrevocable guarantee provided by Tata Realty & Infrastructure Ltd (“TRIL”)

- The guarantee covers the entire principal and interest obligation on the NCDs

- Moreover, TRIL's rating continues to remain underpinned by the strong managerial and financial support provided to it by Tata Sons, given its strategic importance to the Tata group

Shriram Transport Finance Company Ltd. (STFCL; CRISIL AA+)

- Shriram Transport Finance Co. Ltd.’s (STFCL) credit assessment factors in its established presence for almost four decades in the pre-owned CV financing business.

- In this segment, STFCL has created a strong and sustainable competitive advantage through deep understanding of the borrower profile and their credit behavior.

- STFCL's capitalization remains comfortable, given its demonstrated ability to access markets and steady accretion of profits.

- The overall capitalization has further improved, as the company did a Rs.1500 QIP in fiscal 2021, to create additional cushion/buffers to meet any asset side risk from COVID.

- The overall collection efficiency of the company has improved over the months of moratorium, and post moratorium, it has reached 95% of pre-COVID levels. In addition, the company anticipated only 2.5-3% of the book to require re-structuring.

- STFCL has an improving, resource profile which remains well diversified across various funding avenues.

- Ability to diversify resource profile and maintain competitive borrowing cost will remain key monitorables over the medium term

JK Cement (CARE AA, CARE A1+)

- Established market position in North India

- Apart from Grey Cement JK Cement also manufactures White cement and wall putty where operating margins are superior resulting in higher profitability (EBITDA per tonne)

- Strategic location its plants ensures competitive freight cost, as compared to other industry players. Furthermore, proximity to raw materials, self-sufficiency in power and competitive freight costs will continue to ensure high cost efficiency for JK Cement over the medium term.

- Improving demand supply situation in key markets (North India), will continue to support the overall business risk profile.

- Financial risk profile is adequate with Debt/EBITDA less than 3x, with completion of the project-related capex and gradual ramp up of capacities, debt levels and overall capital structure are expected to improve over the medium term.

- JKLC's liquidity is strong as is evident in high liquidity maintained over the past few years and expectations of maintaining the similar levels going forward also, to tide over any adversity, considering cyclical nature of the cement industry.

Indostar Capital Finance Ltd. (IND AA-, IND A1+)

- IndoStar Capital Finance Ltd. (Indostar), is a systemically important, non-deposit taking NBFC, focused on retail lending (forming 73% of AUM; primarily in vehicle financing, SME and Housing Finance segment).

- The company was founded and incorporated by private equity players (Everstone, Goldman Sachs Baer Capital Partners, ACPI Investment managers, and CDIB International). In May 2020, Brookfield invested Rs 1,225 crore and became the largest shareholder and co-promoter.

- Post Brookfield infusion (of Rs.1225 crore) and subsequent open market offer, its holds majority stake in the company of 52.3%, further strengthening the strong institutional backing the company enjoyed in the past.

- With the infusion, the overall capitalization has significantly improved along with providing a strong liquidity buffer to the company.

- Over the last few years, the company has focused on adding granular retail assets and thereby added assets in vehicle financing, SME and Housing Finance. Consequently, wholesale financing (includes structured exposures to small and mid-sized corporates and to established real estate developers in Tier I cities) has reduced over the past few years.

- The share of retail loans in the overall portfolio has increased to 73% of AUM as on September 30, 2020, from 12% as on March 31, 2017, driven by growth in the retail book and contraction of the wholesale portfolio.

Northern ARC Capital Limited (NACL; ICRA A+, ICRA A1+)

- Credit evaluation for NACL derives strength from its established position in providing financing and other solutions to more than 180 entities dealing in niche segments such as Micro Finance, Affordable Housing, used vehicles financing.

- NACL also derives comfort from its strong institutional investors backing (Standard Chartered PE, Fidelity PE, Leapfrog Investments, SMBC) with track record of regular equity infusion.

- The regular capital infusion has led to strong capitalization (Financial leverage is <2x) and comfortable capital adequacy for the company.

- Moreover, NACLs evaluation also draws comfort from NACL’s established investor relationships and its demonstrated fund-raising ability.

- NACL has a comfortable liquidity position however (cash is 15% of total assets), in view of the continuing tightness in market liquidity conditions, especially for NBFCs, the ability of the company to maintain adequate liquidity buffers and secure longer-tenure borrowings will be a key monitorable.

Narmada Wind Energy Private Limited (CARE A+(SO))

- Credit enhancement in the form of irrevocable and unconditional co-obligor guarantee structure provided by various SPVs housing 10 operating projects

- Strong operational track record of projects with diversification in terms of mix of wind and solar projects, geographical diversifications and exposure to more than 10 counter- parties yields stability to cash flows

- Structural features provide liquidity buffer to address delay in payment collections

- Long-term off take arrangement with 40% capacity contracted with strong offtake in form of AAA rated government entities.

- Credit enhancement provided by strong sponsor (Renew Power Ventures Limited; rated A+) in form of corporate guarantee for 30% of NCD amount

- Increase in receivables and dispute by AP discoms to reduce tariff on already contracted PPAs remains key concern

Product Labelling & Disclaimers

| Fund Name | Riskometer | Product Labelling |

| Axis Strategic Bond Fund |  | This product is suitable for investors who are seeking*

|

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Disclaimer

Source: Axis AMC Internal Analysis, Company financials

Data updated as on January 31st 2021. Please refer to the Scheme Information document of the document for detailed asset allocation and investment strategy. Portfolio Allocation is based on the prevailing market conditions and is subject to changes depending on the fund manager’s view of the markets. Sector(s) / Stock(s) / Issuer(s) / Top instruments with increased or decreased exposure mentioned above are for the purpose of disclosure of the portfolio of the Scheme(s) and should not be construed as recommendation to buy/sell/ hold. The fund manager(s) may or may not choose to hold the instruments mentioned, from time to time. The material is prepared for general communication and should not be treated as research report. The data used in this material is obtained by Axis AMC from the sources which it considers reliable. For portfolio details of the scheme as on April 30, 2020, please refer to our website https://web-cug.axismf.com. Investors are requested to consult their financial advisors for any investment decisions.

Statutory Details: Axis Mutual Fund has been established as a Trust under the Indian Trusts Act, 1882, sponsored by Axis Bank Ltd. (liability restricted to Rs. 1 Lakh).

Trustee: Axis Mutual Fund Trustee Ltd.

Investment Manager: Axis Asset Management Co. Ltd. (the AMC)

Risk Factors: Axis Bank Ltd is not liable or responsible for any loss or shortfall resulting from the operation of the scheme. This document represents the views of Axis Asset Management Co. Ltd. and must not be taken as the basis for an investment decision. Neither Axis Mutual Fund, Axis Mutual Fund Trustee Ltd nor Axis Asset Management Company Ltd, its Directors or associates shall be liable for any damages including lost revenue or lost profits that may arise from the use of the information contained herein. No representation or warranty is made as to the accuracy, completeness or fairness of the information and opinions contained herein. The AMC reserves the right to make modifications and alterations to this statement as may be required from time to time.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Copyrights ![]() 2020. All rights reserved Axis Mutual Fund.

2020. All rights reserved Axis Mutual Fund.

Privacy | Terms | Disclaimer | Sitemap