Fund Focus - Axis Banking & PSU Debt Fund

Axis Banking & PSU Debt Fund – Recap

- In 2018, as the NBFC crisis broke out, the interest rate scenario turned opportunistic

- We introduced a 3.5-year corporate bond strategy in our Axis Banking & PSU Debt Fund.

- The strategy offered a high quality portfolio and defined ‘carry’ potential in times of extreme uncertainty.

- Was ideally suited for investors looking to navigate the prevailing interest rate volatility.

Current Positioning

- Repositioning likely over the next quarter.

- Incremental flows, accruals and maturities are deployed in bank CD’s and residual maturity bonds.

- Global headwinds and inflation have driven market yields materially higher. Markets extremely volatile.

- As markets settle, we are looking forward to attractive redeployment opportunities in the 3-5-year segment over the next few months.

Debt Quants

Debt Quants

The yield to maturity should not be taken as an indication of the returns that maybe generated by the fund and the securities bought by the fund may or may not be held till their respective maturities. Data as of 31st May 2022.

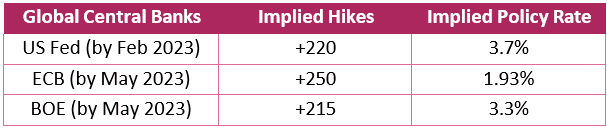

Current Interest Rate Environment

The last 3 months have seen monetary policy responding to brutal inflation pressures. As global central banks attempt to combat runaway inflation, global debt markets have priced in sharp rate hikes. Off cycle monetary meets and surprise rate hikes have kept markets volatile.

Current Interest Rates Environment

Source: Bloomberg, Respective central bank statements, Axis MF Research. Data as of 16th June 2022

Domestic markets echo similar sentiments as bond markets in India have priced in terminal policy rates closer to 6.5%-7.75% from the current repo rate of 4.9%. Swap markets are pricing even higher aggressive rate hikes with implied policy rate expectations of 7% over next 12-18 months. We believe the swap market fears are overdone and should see some correction over the next few months.

RBI Hike and policy Rate

Source: Bloomberg, Axis MF Research. Data as of 16th June 2022

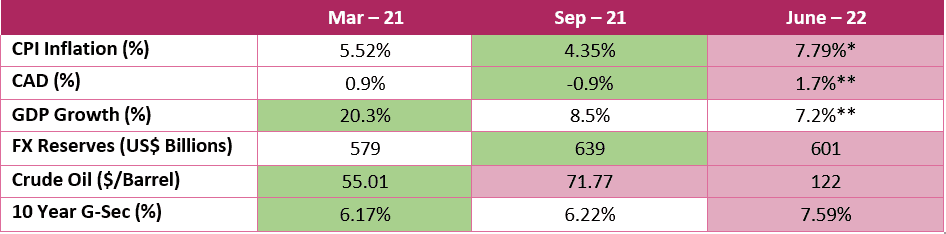

Macro Snapshot

CPI Inflation - April 2022

Source: Bloomberg, Axis MF Research. Data as of 16th June 2022. *CPI Inflation for April 2022. **Values for June 2022 represent RBI projected numbers FY 2022-23

In India too, monetary policy stance has a clear inflation focus. The RBI has effectively raised policy rates by 130 bps (90bps repo + 40bps narrowing of corridor) over the last few months. The central bank has also reversed much of the post covid liquidity accommodation. Markets have already corrected materially, trending high inflation rates and pricing real positive rates. In essence, following the RBI projections of medium term inflation target of 6.7%, markets have already priced in a terminal repo rate (as evidenced by the steep yield curve and OIS rates) above 6.50-6.75% over the next 12-18 months.

Rising global bond yields have had a disproportionate impact on emerging markets. High forex cushion and stronger economic momentum have helped India weather turbulent economic conditions better than other EM countries. However, interest rates have adjusted to the new economic reality.

Yields movement in G-Secs across the curve

Yields movement in G-Sec across curve

Source: Bloomberg, Axis MF Research. Yields are not an indication of returns.

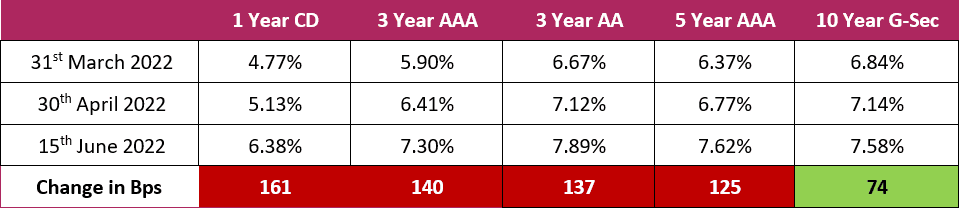

Corporate Bond Markets

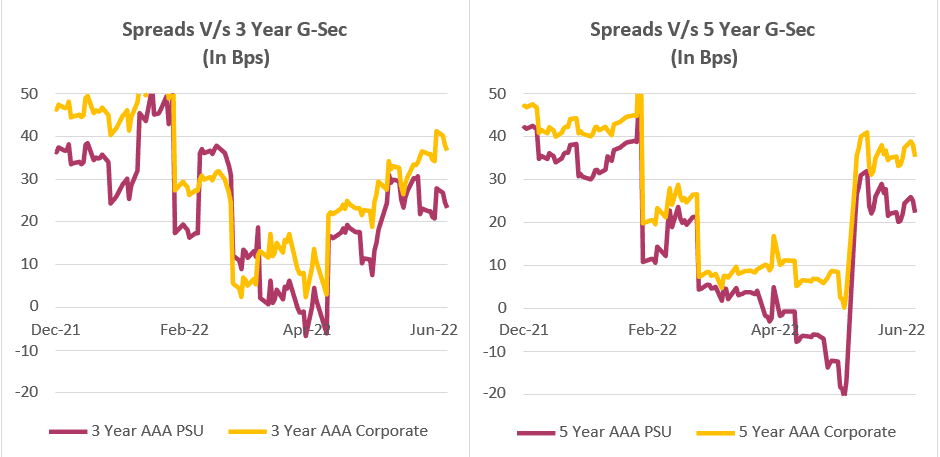

The rise in yields has not cascaded proportionately to the corporate bond market. The has resulted in spreads across the 3-5-year segment narrowing v/s comparable G-Sec rates. Over the last few days (Refer chart below) Corporate bonds and credit spreads have started adjusting to higher benchmark rates.

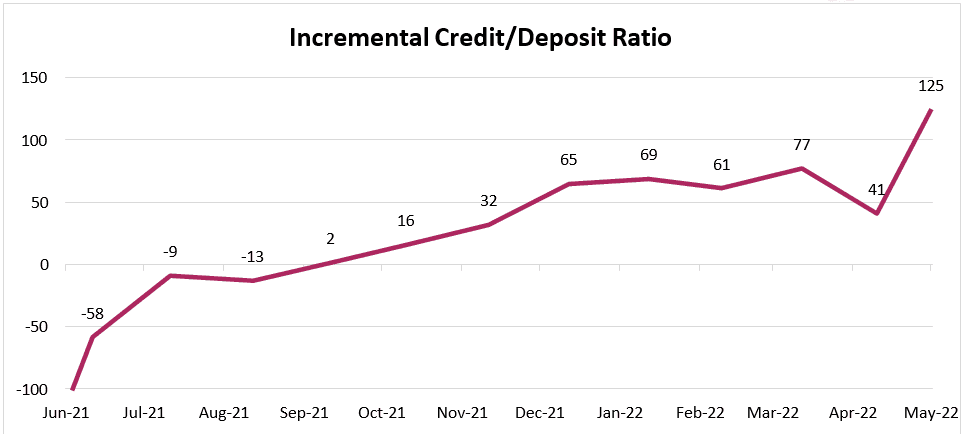

Data from the RBI suggests, incremental credit growth in the system has seen a dramatic rise v/s deposits. Incremental credit to deposit ratio stood at 124.88, the highest since 2019. Faster credit growth over deposit growth is a leading indicator for incremental debt issuances especially by banks & financial institutions. As banks issue credit to corporates and retail customers, slower growth in their deposit bases would compel them to meet additional demand via market borrowings.

Further, with rising deposit rates, we envisage the corporate curve moving incrementally higher from current levels. Additional supply is also likely to put upward pressures on yields.

Incremental Credit/Deposit Ratio [

Source: RBI, Bloomberg, Axis MF Research. Data as of 15th June 2022

Adding all these headwinds together, stance changes on liquidity, fast tracking of neutralizing liquidity renewed demand for credit are likely to have an impact on corporate spreads especially AAA V/s G-Sec. We believe the corporate curve is likely to continue its correction over the next few months which could lead to incremental opportunities for investors especially in the 3-5-year segment as we look to redeploy portfolios closer to the current strategy maturity.

Spreads V/s Year G-Secv

Source: Bloomberg, Axis MF Research. Data as of 15th June 2022

Way forward & Conclusion

To summarize, the bond markets face the following headwinds over the next few months

- Volatility in Yields – Driven by global interest rates and monetary policy action

- Inflation – Impact of commodities, monsoons & domestic price factors

- Fiscal concerns and potential additional government borrowing

- Corporate Bond Supply – Case for normalization of rising spreads between corporate AAA curve & G-Sec curve

The above factors, in our opinion, are key triggers for domestic interest rates to rise in the near term. For the Axis Banking & PSU Debt fund, rising rates will likely offer attractive reinvestment opportunities as the portfolio instruments approach maturity over the next few months. In the interim, as a prudent measure, the fund will continue with its existing holdings and hold off on repositioning the portfolio. As the blocks fall into place naturally, investors are likely to benefit from a clean transition into the next rate cycle without switching portfolios.

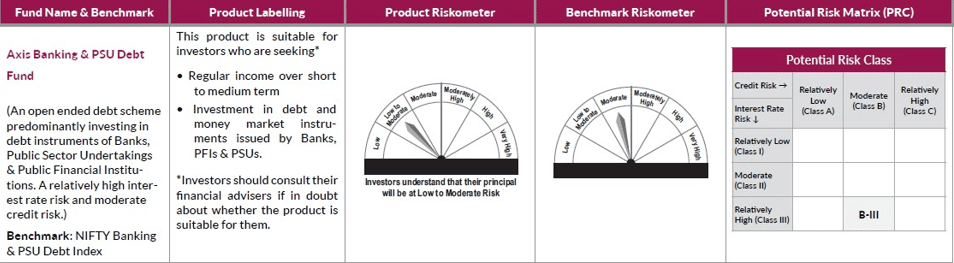

Product Labelling

Product labelling - Axis PSU Debt Fund

Disclaimer

Source of Data: Bloomberg, Axis MF Research. Data as of 15th June 2022.

This document represents the views of Axis Asset Management Co. Ltd. and must not be taken as the basis for an investment decision. Neither Axis Mutual Fund, Axis Mutual Fund Trustee Limited nor Axis Asset Management Company Limited, its Directors or associates shall be liable for any damages including lost revenue or lost profits that may arise from the use of the information contained herein. No representation or warranty is made as to the accuracy, completeness or fairness of the information and opinions contained herein. The material is prepared for general communication and should not be treated as research report. The data used in this material is obtained by Axis AMC from the sources which it considers reliable.

While utmost care has been exercised while preparing this document, Axis AMC does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Investors are requested to consult their financial, tax and other advisors before taking any investment decision(s). The AMC reserves the right to make modifications and alterations to this statement as may be required from time to time.

Statutory details: Axis Mutual Fund has been established as a Trust under the Indian Trusts Act, 1882, sponsored by Axis Bank Ltd. (liability restricted to Rs. 1 Lakh). Trustee: Axis Mutual Fund Trustee Ltd. Investment Manager: Axis Asset Management Co. Ltd. (the AMC) Risk Factors: Axis Bank Limited is not liable or responsible for any loss or shortfall resulting from the operation of the scheme.

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Copyrights ![]() 2020. All rights reserved Axis Mutual Fund.

2020. All rights reserved Axis Mutual Fund.

Privacy | Terms | Disclaimer | Sitemap