5 Mistakes Couples Make With Their Retirement Planning

Retirement is a stage where people are keen on leading a relaxed lifestyle. If you are married and haven’t yet discussed retirement with your spouse, it is better that you do so at the earliest. That’s because you and your spouse may have different aspirations as to how to spend your golden years. And if you want to make sure that you have enough savings for you and your spouse when you retire, you both need to sit down and together discuss how you plan on spending life after 60.

Here are 5 mistakes that couples make with retirement planning, which you shouldn’t:

- Fail to talk about what is expected from each other

As parents, couples spend most of their years raising their children. They are so occupied in nurturing that they do not think about what they will do in the absence of their children. So when the kids grow up and get married or start living separately, couples usually find themselves in a position they didn’t prepare themselves to be in. And there is a possibility that both of them have a different perspective on how to live their retired life. If either of them haven’t saved enough to fulfil their goals, this can lead to misunderstanding between. For example, you may have thought of venturing on a world tour while your spouse may have had thoughts of retiring in a quiet countryside home. So to make sure that both of you are on the same page, talk about your retirement plans while you are young.

- You feel it’s too late to start investing for retirement

Now if you and your partner did not pay enough importance to retirement when you both were young and feel that now it is too late to raise a retirement fund, you can actually do it. There are multiple schemes out there that allow investors to invest according to their risk appetite and investment horizon. Depending on the years you have left for retirement, pick a scheme. Better late, than never.

- Fail to be realistic about your retirement corpus

Having a realistic corpus figure is essential. Couples should not try to replicate the retirement corpus of their friends or neighbours. When you set realistic goals, finding lucrative schemes may become easier than anticipated. But if you chase a baseless retirement corpus figure, you may not be able to achieve anything in the long run.

- Fail to make a proper financial plan

Financial planning is the act of determining your short term and long term goals so that you are able to spread your investments in a smarter way. If you and your spouse failed to make a financial plan and prioritize your goals, you may end up exhausting your savings at a young age, leaving you bankrupt during your sunset years.

- Not building an emergency fund

Failing to plan an emergency fund for the life’s most unexpected moments can lead to exhaustion of all your savings. An exigency can not only eat your savings, but it may also force you to break your other investments as well. So if you want to make sure that your long term investments remain unharmed, build an emergency fund using a liquid fund so that neither your or your spouse will have to exhaust their savings in case of a financial emergency.

If you or your spouse haven’t yet invested in a retirement scheme and are looking for a lucrative scheme, you can consider investing in Axis Retirement Fund.

Axis Retirement Fund is An open-ended retirement solution oriented scheme having a lock-in of 5 years or till retirement age (whichever is earlier) . Its objective is to provide long-term capital appreciation / income by investing in a mix of equity, debt and other instruments to help investors meet their retirement goals

Axis Retirement Fund offers three investment plans -

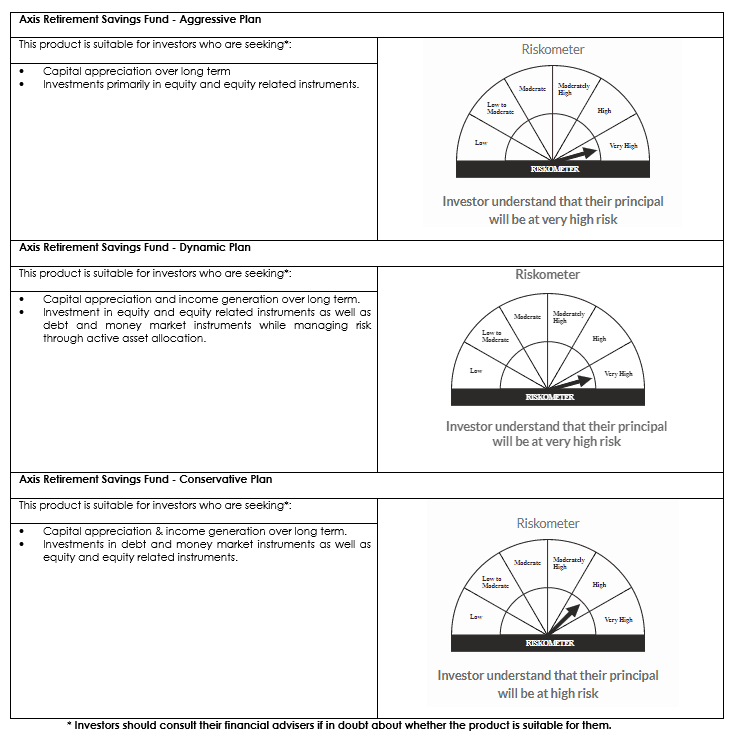

Axis Retirement Fund - Aggressive Plan: Aggressive plan can be opted by investors who are seeking capital appreciation with a long term investment objective. Here investments are predominantly made in equity and equity-related instruments as well as debt, money market instruments, Gold ETFs and units of REITs and InvITs. Investors who plan to opt for the Aggressive Plan can expect equity exposure anywhere from 65% to 80%.

Axis Retirement Fund - Dynamic Plan: Dynamic investment plan is brought into effect with a dual objective. Axis Retirement Fund - Dynamic Plan can generate capital appreciation by investing in equity and equity-related securities as well as generate income by investing in debt and money market securities. It manages to do this while attempting to manage risk from the market through active asset allocation. The Investment Plan may also invest in units of Gold ETF or units of REITs & InvITs.

Axis Retirement Fund - Conservative Plan: Conservative investment plan by Axis Mutual Funds hopes to generate regular income through investments majorly in debt and money market instruments and to generate long term capital appreciation by investing a certain portion of the portfolio in equity and equity-related securities. Axis Retirement Fund - Conservative Plan may also invest in units of Gold ETF or units of REITs & InvITs.

Before investing in Axis Retirement Fund, investors should determine their risk appetite. This might help them in making an informed investment decision.

Axis Retirement Fund

(An open-ended retirement solution oriented scheme

having a lock-in of 5 years or till retirement age (whichever is earlier)).

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Copyrights ![]() 2020. All rights reserved Axis Mutual Fund.

2020. All rights reserved Axis Mutual Fund.

Privacy | Terms | Disclaimer | Sitemap